Teachers' Retirement System (TRS)

Connecticut's Teachers' Retirement System (TRS), one of the State's largest retirement systems, is a "defined benefit plan" administered by the Teachers' Retirement Board. A defined benefit plan means, upon retirement, an eligible teacher participating in the TRS will receive a fixed pension benefit that is determined by the number of years the individual taught in Connecticut public schools and the individual's final average salary.

Since 1939, the TRS has provided retirement benefits to its members. However, for much of the system's history, the State did not properly save for the retirement benefits promised to teachers participating in the TRS. Instead of "pre-funding," or contributing to an employee's pension benefits from the beginning and entirety of his/her employment, the State of Connecticut used a “pay-as-you-go” approach and paid pension benefits to retired teachers as they came due through annual appropriations.

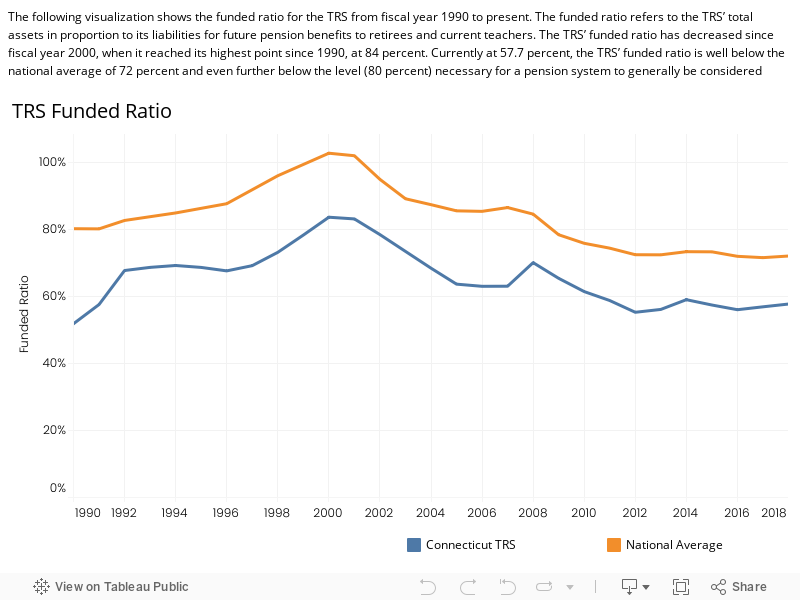

As a result of this practice, and several other critical factors, the TRS has accumulated more than $13.1 billion in unfunded liabilities and is currently considered a poorly-funded pension system with a funded ratio among the worst in the nation at only 57.7 percent. The funded ratio refers to the TRS’ total assets in proportion to its liabilities for future pension benefits to retirees and current teachers.

Three primary factors have driven the TRS' unfunded liability problems:

1. Years of No State Contributions

Prior to 1979, retirement benefits earned by TRS members were completely unfunded by the State of Connecticut. While participating teachers made contributions from their paychecks (and currently contribute six percent of their annual salaries), the State did not begin pre-funding the TRS until 1982. Although the State began pre-funding 35 years ago, the impacts of its years of no contributions to the TRS are still being felt. More than $4 billion (38 percent) of the TRS' total unfunded liability in fiscal year 2014 was attributable to the State not contributing to the pension system for 40 years.

2. State Contributions Often Fell Short

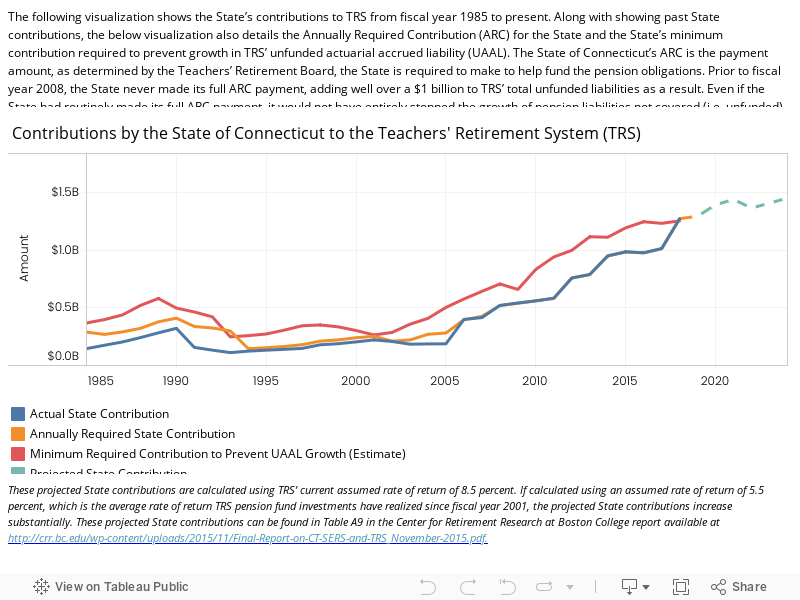

Once the State did begin making contributions to the TRS, it often did not make its full annually required contribution (ARC). Beginning in 1979 with a contribution of 35 percent of its ARC, the State was required to gradually increased the portion of its ARC it would contribute to the TRS until 1993 when the State was expected to make its full contribution. However, not only did the State fall short of contributing its scheduled payments multiple times prior to 1993, but it failed to make its full ARC until 2008. While the State has made its full ARC every year since 2008, as required according to the pension obligation bonds the State issued that year, its underfunded contributions added $1.5 billion to the TRS' total unfunded liabilities by fiscal year 2014.

3. Assumed Returns Have Been Overly Optimistic in Recent Years

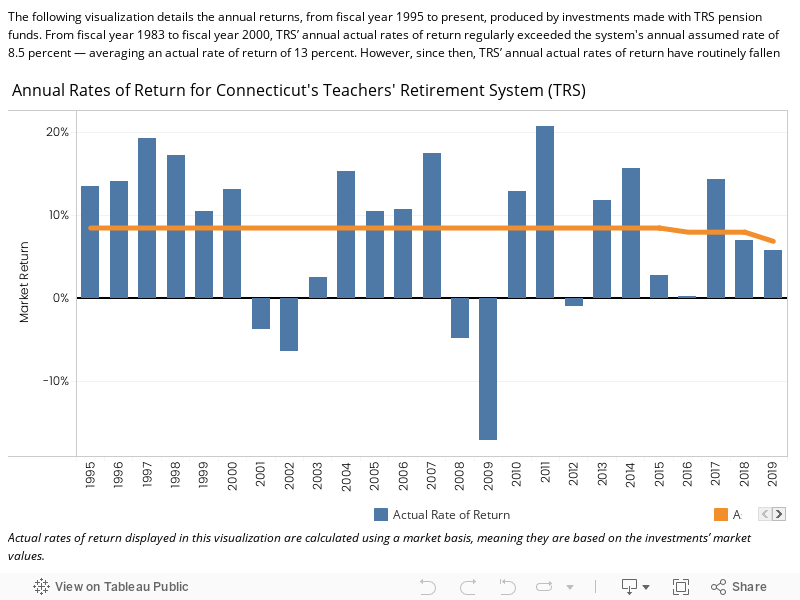

The TRS' unfunded liability has also increased over the years as a result of investments made with TRS' pension funds failing to meet their assumed rates of return. From fiscal year 1983 to fiscal year 2000, investments made with TRS' pension funds regularly produced return rates higher than the system's assumed rate of 8.5 percent. During this time, the TRS averaged an annual actual rate of return of 13 percent — 4.5 percentage points higher than its assumed rate. These higher than assumed rates of return lowered the TRS' unfunded liabilities. However, since fiscal year 2001, the TRS' annual actual rate of return has fallen short of its assumed rate 10 times, and its average actual rate of return has been 6.1 percent. As a result of these return shortfalls, the TRS' unfunded liabilities have increased by billions of dollars. Although lower actual rates of return have been more frequently realized in recent years, the TRS' assumed rate of return remained unchanged at 8.5 percent until fiscal year 2016 when it was lowered to 8.0 percent. In 2019, the assumed rate of return for the TRS was lowered to 6.9 percent, however, this figure is still significantly higher than the three or four percent assumed rate that many in academia and the financial sector argue is more realistic since the Great Recession.